Fuel Grade Petcoke Market Scope and Key Industry Developments 2032

The Fuel Grade Petcoke Market continues to demonstrate stable expansion as industries worldwide seek cost-effective, high-calorific-value fuel alternatives. Valued at USD 14,123.42 million in 2024, the market is projected to grow at a CAGR of 5.7% from 2025 to 2032. The increasing demand from energy-intensive industries such as cement, power generation, and steel manufacturing, coupled with the rising availability of petroleum coke as a refinery by-product, is driving sustained market growth. Comprehensive insights into competitive dynamics, regional trends, and future outlook are detailed in the latest market report.

High Energy Content Drives Industrial Adoption

Fuel grade petroleum coke (petcoke) is a carbon-rich solid material derived from oil refining processes. Known for its high calorific value and low cost compared to coal, fuel grade petcoke is widely used as a substitute fuel in industrial boilers and kilns. Its ability to deliver consistent heat output makes it particularly suitable for cement kilns, power plants, and metallurgical operations.

As global industrialization accelerates—especially in emerging economies—manufacturers are prioritizing fuel efficiency and cost reduction. Fuel grade petcoke offers a competitive advantage by lowering operational fuel expenses while maintaining high thermal efficiency, making it a preferred choice across multiple heavy industries.

Market Segmentation by Type Reflects Diverse Industrial Needs

The fuel grade petcoke market is segmented by type into sponge coke, purge coke, shot coke, and needle coke. Among these, sponge coke holds a significant market share due to its porous structure and high carbon content, which enhance combustion efficiency. It is widely used in cement kilns and power generation facilities.

Shot coke, characterized by its spherical shape and dense structure, is commonly utilized in applications requiring stable and controlled burning. Purge coke serves niche industrial applications, while needle coke—although more frequently associated with anode production—also finds limited use as a specialized fuel grade product in high-performance applications.

This diversity in petcoke types allows end users to select fuel grades based on specific combustion, emission, and cost requirements.

Applications Across Energy-Intensive Industries

Fuel grade petcoke is extensively used across various applications, including power generation, cement manufacturing, steel production, and other industrial heating processes. The cement industry remains the largest consumer, driven by the material’s ability to achieve high kiln temperatures essential for clinker production.

Power plants increasingly rely on petcoke as a supplementary or alternative fuel, particularly in regions with abundant refinery outputs. In steel manufacturing, petcoke supports high-temperature processes while contributing to operational cost efficiency. Other applications include brick kilns, lime production, and industrial boilers, where consistent heat supply is critical.

End-User Industries Drive Long-Term Demand

End users of fuel grade petcoke primarily include cement manufacturers, power utilities, metallurgical companies, and industrial processing plants. Cement producers dominate consumption due to the material’s compatibility with rotary kilns and its cost advantage over traditional fuels.

Power generation companies are adopting petcoke blends to optimize fuel costs, especially in countries where coal prices fluctuate. Industrial manufacturers, including chemical and glass producers, also utilize petcoke to meet high-temperature energy requirements.

The continued expansion of infrastructure projects, urban development, and manufacturing capacity—particularly in Asia-Pacific and the Middle East—is expected to support steady demand across end-user segments.

Regional Trends Highlight Emerging Market Growth

Geographically, Asia-Pacific represents a major growth hub for the fuel grade petcoke market, driven by rapid industrialization in countries such as China, India, and Southeast Asian nations. Increasing cement production, expanding power capacity, and rising refinery operations contribute significantly to regional demand.

North America maintains a strong market presence due to high refinery output and established industrial infrastructure. The Middle East benefits from abundant crude oil refining capacity, positioning the region as both a major producer and consumer of petcoke. Meanwhile, Latin America and Africa are witnessing gradual adoption as industrial development accelerates.

Environmental regulations vary by region, influencing adoption rates and driving investments in emission-control technologies.

Environmental Considerations and Regulatory Landscape

Despite its economic advantages, fuel grade petcoke faces scrutiny due to its high sulfur content and carbon emissions. Governments and environmental agencies are implementing stricter emission standards, particularly in developed regions. As a result, industries are increasingly investing in advanced filtration systems, flue gas desulfurization units, and cleaner combustion technologies to mitigate environmental impact.

In developing economies, regulatory frameworks are evolving, balancing industrial growth with environmental sustainability. These measures are shaping how petcoke is sourced, processed, and consumed across global markets.

Competitive Landscape: Established Energy Giants Lead the Market

The global fuel grade petcoke market is characterized by the presence of major oil and energy corporations with integrated refining operations. Key players include BP Plc, Chevron Corporation, Essar Oil Ltd., ExxonMobil Corporation, and HPCL–Mittal Energy Limited. These companies benefit from strong supply chains, extensive refinery networks, and long-term contracts with industrial consumers.

Strategic initiatives such as capacity expansion, supply agreements, and investments in cleaner fuel technologies help companies maintain competitive positioning. Partnerships with cement and power producers further strengthen market penetration.

Future Outlook: Stable Growth with Strategic Adaptation

The fuel grade petcoke market is expected to maintain steady growth through 2032, supported by industrial expansion, infrastructure development, and demand for economical energy sources. While environmental challenges persist, technological advancements and regulatory compliance strategies will play a key role in sustaining market viability.

As industries seek to balance cost efficiency with sustainability, fuel grade petcoke will remain a critical component of the global industrial fuel mix.

For detailed market segmentation, regional analysis, and forecast methodology, stakeholders can access a sample of the Fuel Grade Petcoke Market report to gain comprehensive insights and data-driven perspectives.

Browse more Report:

Preoperative Infection Prevention & Wound Cleansing Devices Market

Catégories

Lire la suite

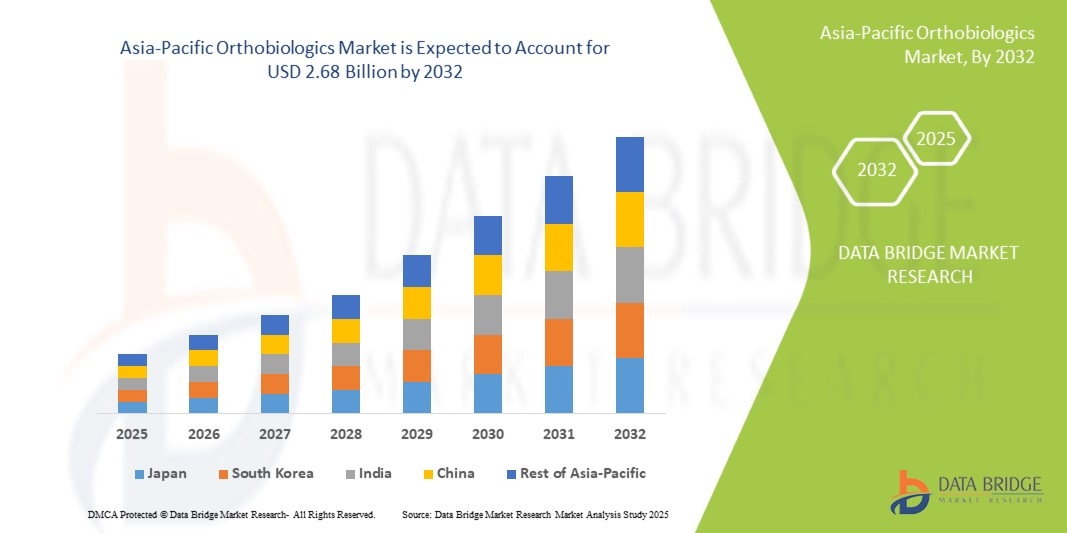

"Latest Insights on Executive Summary Asia-Pacific Orthobiologics Market Market Share and Size CAGR Value The Asia-Pacific Orthobiologics Market was valued at USD 1.8 Billion in 2024 and is expected to reach USD 2.68 Billion by 2032, at a CAGR of 5.1% during the forecast period. Asia-Pacific Orthobiologics Market Market report presents...

Seattle's Most Prolific Bank Robber In the 1990s one man carried out nearly two dozen bank heists across Seattle, walking away with millions. He relied on elaborate makeup and facial prosthetics to conceal his identity, a disguise that led the press to dub him "Hollywood". Repeated attempts by law enforcement to catch him faltered, turning the pursuit into a long-running investigation. A new...

The Wikimedia Foundation, the organization responsible for Wikipedia, has faced a setback in its legal efforts to challenge the Online Safety Act. Despite this loss, the foundation remains hopeful about resisting certain provisions, particularly mandatory age verification measures. On August 11, 2025, the High Court in London dismissed a judicial review initiated by Wikimedia in May, which...

Hoyoverse hat die Veröffentlichung einer Xbox-Version ihres Action-Rollenspiels Zenless Zone Zero bestätigt. Das Spiel wird im Juni 2025 erscheinen und dabei die Version 2.0 sowie speziell auf Xbox Series X/S abgestimmte Optimierungen mitbringen. Die Umsetzung erfolgt voraussichtlich im Sommer nächsten Jahres, wobei auch eine Version für Xbox Cloud Gaming geplant ist, sodass...

Sexual wellness education is one of the most influential forces shaping consumer attitudes in India, especially among younger buyers. Increasing awareness about safe sex practices, pleasure, consent, and reproductive health directly impacts purchasing trends. Consequently, the idea of the best condoms in india 2022 is closely tied to user awareness, accessibility of information, and comfort...