robotics system integration Market Share Key Players Redefining Robotics Adoption Globally

The robotics system integration market share is increasingly dominated by key players specializing in industrial automation and robotic solutions. Leading companies are leveraging their expertise in system design, software integration, and maintenance services to capture a significant portion of the market. With the rise of collaborative and smart factory solutions, smaller players are also gaining traction, contributing to a more competitive landscape.

The Robotics System Integration Market has emerged as a cornerstone of modern industrial automation. With industries increasingly adopting robotics to enhance operational efficiency, reduce human errors, and improve production consistency, system integration plays a crucial role in ensuring that robotic systems work seamlessly with existing infrastructure. Robotics system integration encompasses the design, deployment, and management of robots, combining hardware, software, and control systems into cohesive operational units tailored to specific industrial needs.

Market Overview

The robotics system integration market has witnessed substantial growth over the past decade, driven by the growing demand for automation across diverse sectors. Key industries such as automotive, electronics, aerospace, and healthcare are increasingly investing in robotic solutions to improve productivity and reduce labor-intensive processes. By integrating robotics systems into production lines, companies can streamline operations, optimize workflow, and maintain high-quality standards. The market’s expansion is also supported by technological advancements in artificial intelligence (AI), machine learning, and the Internet of Things (IoT), which have enhanced robots' adaptability and performance in complex industrial environments.

Market Dynamics

The market dynamics of robotics system integration are shaped by a combination of drivers, restraints, opportunities, and challenges. One of the primary drivers is the rising need for efficiency and cost-effectiveness in manufacturing processes. Robotics system integration allows manufacturers to automate repetitive and dangerous tasks, minimizing workplace accidents while boosting productivity. Additionally, the increasing demand for smart factories and Industry 4.0 solutions has fueled the adoption of integrated robotic systems that can communicate with other machines and software platforms, enabling real-time monitoring and data-driven decision-making.

On the other hand, high initial costs and the complexity of integrating advanced robotic systems with existing infrastructure pose significant challenges. Many small and medium-sized enterprises (SMEs) find it difficult to invest in full-scale automation due to financial constraints. Moreover, the shortage of skilled professionals capable of designing, implementing, and maintaining integrated robotic systems slows down market adoption, particularly in emerging economies.

Drivers of Growth

Several factors are driving the growth of the robotics system integration market. First, the push for operational efficiency and productivity across industries is prompting companies to adopt robotics solutions. Robots can operate continuously without fatigue, maintain precision in repetitive tasks, and ensure consistent product quality, which is difficult to achieve through manual labor alone.

Second, the increasing adoption of collaborative robots, or cobots, is transforming the industrial automation landscape. Cobots work alongside human operators, complementing human skills while taking over repetitive or physically demanding tasks. This collaboration reduces the risk of injury and allows human workers to focus on more strategic, creative, or problem-solving activities.

Third, technological advancements in AI, machine learning, and computer vision have made robots smarter and more adaptable. Integrated robotic systems can now analyze vast amounts of data, identify patterns, and adjust operations in real time, offering businesses unprecedented operational flexibility and efficiency. These innovations are particularly beneficial in industries such as electronics manufacturing and logistics, where precision, speed, and adaptability are critical.

Market Restraints

Despite its promising growth, the robotics system integration market faces several restraints. The high cost of robotic systems, including hardware, software, and maintenance, is a significant barrier for many companies, especially in developing regions. Additionally, integrating robotics with existing systems requires complex planning and specialized expertise, which may be lacking in certain organizations.

Regulatory challenges also play a role, as different countries have varying standards for industrial automation, safety protocols, and labor laws. Compliance with these regulations adds another layer of complexity to the integration process, increasing the time and cost required for deployment.

Market Segmentation

The robotics system integration market can be segmented based on type, application, end-user industry, and region. In terms of type, the market includes hardware-based integration, software-based integration, and hybrid solutions that combine both. Application-wise, it spans assembly and manufacturing, material handling, welding and painting, inspection and quality control, and logistics and warehouse automation.

The end-user industries driving demand include automotive, electronics, food and beverage, pharmaceuticals, healthcare, and aerospace. Each industry has unique requirements for robotic integration, ranging from precision assembly in electronics to automated material handling in warehouses. Regionally, North America and Europe are leading markets due to advanced technological adoption, while Asia-Pacific is emerging rapidly, fueled by industrial expansion and government initiatives promoting automation.

Challenges and Market Constraints

One of the major challenges facing the market is the integration of legacy systems with new robotic technologies. Many companies still rely on outdated machinery that may not be compatible with modern robotics, requiring significant customization or infrastructure upgrades. Additionally, cybersecurity concerns are becoming increasingly relevant, as integrated robotic systems connected to networks can be vulnerable to cyberattacks, potentially disrupting operations and causing financial losses.

Another constraint is the shortage of skilled workforce capable of implementing, programming, and maintaining integrated robotic systems. Training and retaining talent in robotics and automation is costly and time-consuming, slowing the adoption rate in certain regions.

Future Outlook

The future of the robotics system integration market looks promising, with strong growth projected over the next decade. The ongoing digital transformation and the push for smart factories will continue to drive demand for integrated robotics solutions. Advancements in AI, IoT, and cloud computing will further enhance the capabilities of robots, allowing for more autonomous, efficient, and flexible operations.

Furthermore, as costs of robotic systems decline and more affordable solutions become available, small and medium-sized enterprises will increasingly adopt automation, expanding the market further. Collaborative robots, AI-driven analytics, and predictive maintenance solutions are expected to play a significant role in shaping the next generation of industrial automation.

Multi-Tasking Machine Tools Market Trends

Vacuum Coating Machines Market Trends

Categorii

Citeste mai mult

A second independent validation confirms Surfshark's user-first privacy stance Demonstrating ongoing dedication to transparency, the VPN service undergoes rigorous external scrutiny Prestigious auditor Deloitte, a member of the Big Four, conducted this latest assessment Their findings corroborate the company's claims regarding the non-retention of user usage data This recurring verification...

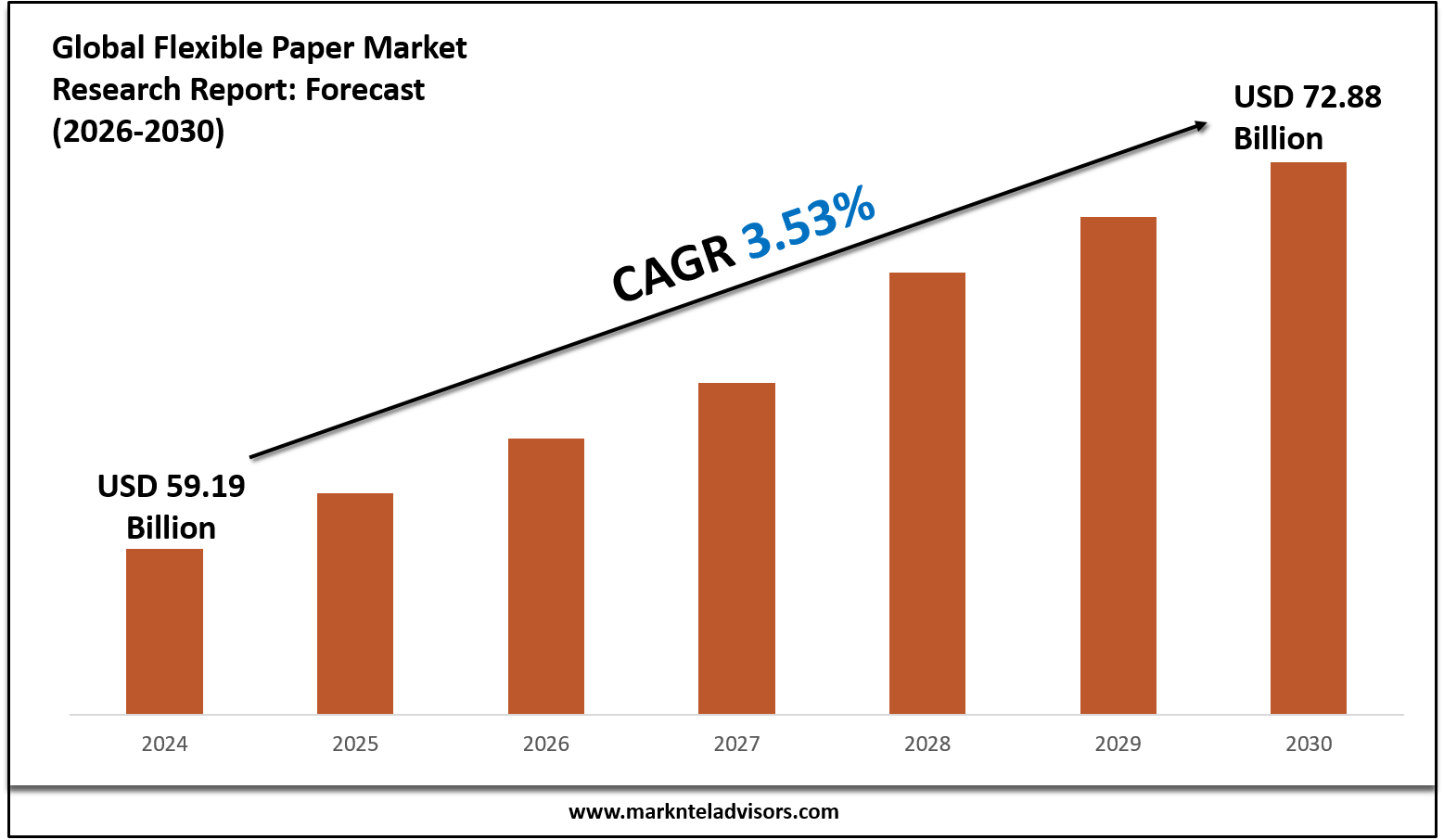

Introduction:The Global Flexible Paper Market, valued at approximately USD 59.19 billion in 2024, is anticipated to reach around USD 72.88 billion by 2030, reflecting a robust compound annual growth rate (CAGR) of 3.53%. This growth is primarily driven by escalating demand for sustainable and eco-friendly packaging solutions, regulatory shifts towards combating plastic usage, and the...

"Future of Executive Summary Asia-Pacific Gas Delivery System for Wafer Fab Equipment Market: Size and Share Dynamics CAGR Value Growing demand form the semiconductors and materials industry especially in the emerging economies, rising up gradation of existing infrastructure with advanced systems and increasing infrastructural development activities are the major factors attributable to the...

Weite Felder erkunden Das Gebiet „Weite Felder“ in Hollow Knight: Silksong präsentiert sich als riesiges und vielfältiges Biom, das Hornet vor neue Herausforderungen stellt. Um voranzukommen, solltest du zunächst nach Shakra Ausschau halten und die Karte erwerben, um den Überblick zu behalten. Nach dem Betreten der Weiten Felder ist es ratsam, sich auf die Suche...

Fondant continues to gain popularity in Europe’s bakery industry, where presentation and creativity are equally important as taste. Rising demand for customized and themed cakes reflects the evolving expectations of consumers who view desserts as an extension of personal expression. Analyzing demand trends shows that convenience and innovation are key drivers. Ready-to-roll fondant is...