hydronic underfloor heating Market Share Strengthening Amid Growing Residential Adoption

In terms of hydronic underfloor heating Market Share, Europe currently leads due to its long-standing adoption of efficient heating systems and strict energy regulations. North America and Asia-Pacific are emerging as fast-growing markets, driven by climate-conscious consumers and increasing construction activities. The market share is also being shaped by technological advancements such as wireless controls and integration with renewable sources like solar heating.

The hydronic underfloor heating market has witnessed significant attention in recent years as homeowners, businesses, and infrastructure projects increasingly focus on energy-efficient and sustainable heating solutions. Unlike conventional heating systems that rely on radiators or forced-air heating, hydronic underfloor heating works by circulating warm water through pipes embedded beneath the floor surface. This method ensures even heat distribution, improved comfort, and reduced energy consumption compared to traditional systems. Growing concerns about carbon emissions and the shift toward renewable and energy-efficient technologies are major factors driving the market. The rise in smart homes, luxury housing projects, and demand for modern heating solutions in both residential and commercial sectors also highlights the relevance of hydronic underfloor heating. With rising awareness of energy conservation and supportive government policies, the market continues to expand, offering a viable alternative to conventional heating systems across the globe.

Market Dynamics

The dynamics of the hydronic underfloor heating market are shaped by multiple factors including technological advancements, changing customer preferences, and government initiatives. The market benefits significantly from its compatibility with energy-efficient boilers, heat pumps, and renewable energy sources such as solar thermal systems. This adaptability makes hydronic underfloor heating suitable for various applications ranging from residential apartments to commercial complexes and industrial facilities. Additionally, the market is heavily influenced by the increasing need for thermal comfort, the growing adoption of green building standards, and the rising emphasis on reducing overall energy costs. On the other hand, high initial installation costs and complex retrofitting processes create barriers for wider adoption. However, innovations in heating components, better installation techniques, and integration with smart thermostats are contributing to a favorable market landscape.

Drivers

Several key drivers are propelling the hydronic underfloor heating market forward. First and foremost is the global demand for energy-efficient solutions. As energy prices rise and governments push for reduced dependency on fossil fuels, hydronic underfloor heating has emerged as a practical choice due to its efficiency in conserving energy. Another major driver is the surge in construction activities, particularly in the residential and commercial sectors, where buyers seek modern and luxurious amenities. Increasing disposable incomes and rising living standards further boost consumer preference for comfort-based systems like underfloor heating. Additionally, government incentives and building codes promoting energy-efficient construction have played a vital role in increasing adoption. The growing integration of renewable energy systems, such as solar thermal energy, with hydronic underfloor heating systems has further enhanced the attractiveness of this market. Collectively, these drivers indicate strong growth potential in the near future.

Restraints

Despite its many advantages, the hydronic underfloor heating market faces certain restraints that hinder widespread adoption. One of the most prominent challenges is the high installation cost compared to conventional heating systems. Since hydronic systems involve intricate pipe layouts, insulation, and specialized labor, the initial investment is significantly higher. This cost factor often discourages homeowners, particularly in developing regions, from adopting the technology. Another major restraint is the complexity of retrofitting existing buildings with hydronic systems. While new constructions can easily accommodate these systems, older buildings require extensive modifications, making the process both expensive and time-consuming. Additionally, the slower response time of hydronic underfloor heating compared to forced-air systems can be a disadvantage in certain climates where quick heating is required. These limitations collectively present challenges for broader market penetration.

Segmentations

The hydronic underfloor heating market can be segmented on the basis of application, installation type, and end-use industry. By application, the market is typically divided into residential, commercial, and industrial segments. The residential segment dominates due to the increasing preference for energy-efficient and comfort-oriented home solutions. In terms of installation type, the market is segmented into new installations and retrofits. New installations hold a larger market share as construction projects can integrate underfloor heating during the building phase more easily. However, the retrofit segment is gaining momentum as consumers increasingly seek upgrades to existing heating systems. Based on end-use, the commercial segment includes office spaces, retail outlets, educational institutions, and healthcare facilities, all of which are adopting underfloor heating for enhanced comfort and energy savings. The industrial segment, though smaller, also contributes with applications in specialized manufacturing units requiring uniform heating.

Challenges and Market Constraints

The hydronic underfloor heating market is not without its share of challenges. Apart from the high installation and retrofitting costs, one major challenge is the lack of awareness among consumers in certain regions about the benefits of underfloor heating. Many potential users continue to rely on traditional systems simply due to familiarity or limited information. Moreover, the market faces supply chain and skilled labor issues, as installation requires specialized expertise. Any shortage of skilled professionals can delay projects and increase costs. In colder climates, another constraint is the relatively longer heating time, which makes hydronic systems less practical for users seeking immediate warmth. Additionally, the market must navigate regulatory complexities as energy policies vary widely across regions, influencing adoption rates differently. Overcoming these constraints will require industry collaboration, better awareness campaigns, and innovations that simplify installation processes while reducing costs.

Future Outlook

The future outlook for the hydronic underfloor heating market appears highly promising, driven by global sustainability goals and advancements in heating technologies. As governments worldwide continue to emphasize net-zero carbon targets, underfloor heating systems are expected to gain further traction due to their compatibility with renewable energy sources and energy-efficient design. The growing trend of smart homes and IoT integration will also play a significant role, as underfloor heating systems become more responsive, controllable, and customizable through smart devices. Additionally, as installation costs decline over time due to improved technologies and economies of scale, the affordability of these systems will improve, thereby expanding their customer base. With increasing urbanization, rising disposable incomes, and expanding construction activities, the hydronic underfloor heating market is set to experience robust growth. Moreover, collaborations between manufacturers, contractors, and energy companies will likely pave the way for innovative solutions that address current challenges while enhancing overall system efficiency.

Categories

Read More

Rhythm + Flow Season 2 Overview The battle arena reopens as Rhythm + Flow prepares to crown hip-hop's next icon. Judging this high-stakes competition: Atlanta's own Ludacris Chart-topping maestro DJ Khaled Rising powerhouse Latto Contestants vie for a $250,000 prize and industry supremacy when Season 2 premieres globally on November 20. Adding explosive firepower to the panel: Rap deity Eminem...

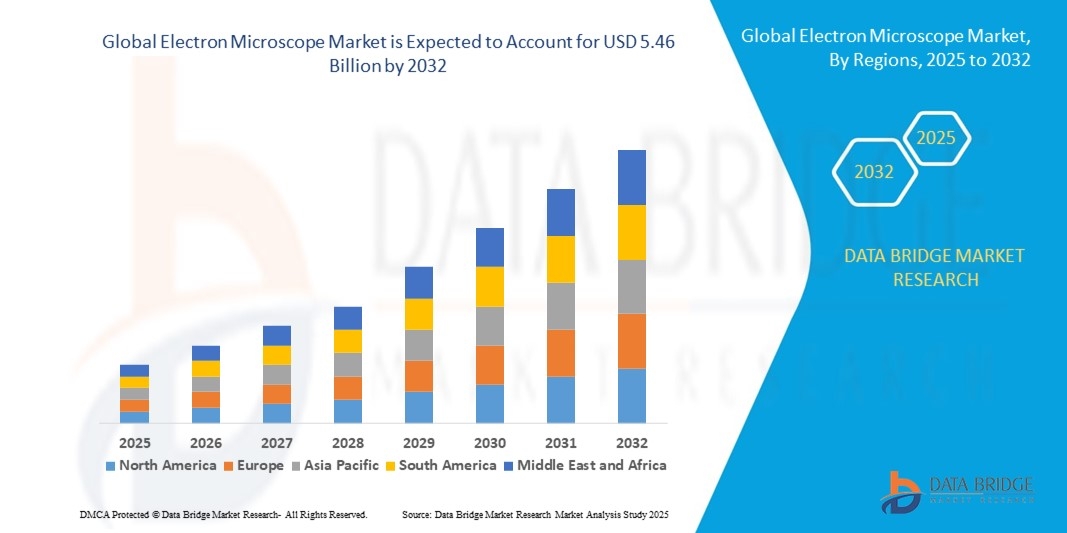

"What’s Fueling Executive Summary Electron Microscope Market Size and Share Growth CAGR Value The global electron microscope market size was valued at USD 3.40 billion in 2024 and is expected to reach USD 5.46 billion by 2032, at a CAGR of 6.10% during the forecast period. Electron Microscope Market research report has been produced with the...

Lizensierungsstatus im Überblick In der aktuellen Ausgabe von FC 26 hat EA Sports erhebliche Anstrengungen unternommen, um die Lizenzlandschaft zu verbessern. Dabei konnten zahlreiche alte Partner zurückgewonnen und neue Kooperationen eingegangen werden, was die Anzahl der lizenzierten Teams, Ligen und Nationalmannschaften deutlich erhöht hat. Insgesamt sind nun über 20.000...

The global leather industry is undergoing transformation, with technological innovations and sustainable practices driving demand for advanced tanning agents. The Tanning Agents Market has become increasingly competitive as manufacturers seek to enhance the quality and durability of leather products while minimizing environmental impact. Tanning agents serve a crucial function in leather...

Krafton, признанная компания, создавшая популярные игры PUBG и Subnautica 2, объявила о масштабных изменениях в своей структуре. В рамках новой стратегии она планирует сосредоточиться на развитии технологий искусственного интеллекта, став компанией с приоритетом на AI. Это означает, что все основные бизнес-процессы и проекты будут интегрированы с использованием продвинутых решений в области...