The Symptomatic Factor: Why Epilepsy Following Brain Injury Accounts for 35% of the Global Treatment Market's Revenue

Within the complex architecture of the global Epilepsy Diagnosis and Treatment Market, one segment stands out as the primary revenue generator: **Symptomatic Epilepsy**. This category, which includes seizures that develop after a recognized brain injury such as a stroke, severe head trauma, brain tumors, or CNS infections, currently accounts for a dominant 35% of the total market revenue. This high percentage is a stark indicator of the significant medical and economic burden associated with acquired neurological damage. Unlike idiopathic epilepsy, where the cause is unknown, symptomatic cases have a clear, identifiable etiology, which often allows for more targeted, albeit often more complex, diagnostic and treatment pathways. The high frequency of these underlying conditions—particularly strokes and head injuries—in the general population ensures a constant flow of patients into this high-revenue segment of the epilepsy market, demanding sophisticated medical interventions.

The dominance of the symptomatic segment is directly reflected in the type of care required. Patients in this category frequently present with refractory or drug-resistant epilepsy, necessitating aggressive and specialized treatment plans. While initial therapy may involve Antiepileptic Drugs (AEDs), the failure rate is often higher than in other epilepsy types, leading to a greater reliance on advanced diagnostics and, critically, surgical interventions. Procedures such as focal resection, laser interstitial thermal therapy (LITT), and the implantation of neuromodulation devices like Vagal Nerve Stimulators (VNS) or Responsive Neurostimulators (RNS) are often reserved for these complex cases. These high-value procedures, coupled with the need for multi-disciplinary care involving neurosurgeons, neurologists, and specialized nurses, contribute disproportionately to the overall market valuation. The economic weight of managing these severe, secondary forms of epilepsy is a major propeller of the industry’s overall growth trajectory, which is projected to reach $17.64 billion by 2035.

Understanding the epidemiology of this segment is crucial for companies focusing on R&D and market strategy. For those interested in the breakdown of the current market segmentation, the full report provides an in-depth analysis of symptomatic, idiopathic, and cryptogenic types. The challenges posed by symptomatic epilepsy have spurred major innovation in both diagnostic imaging and personalized treatment. Advanced magnetic resonance imaging (MRI) techniques, PET scans, and high-density EEG are often employed to precisely locate the epileptogenic zone, which is vital for surgical planning. Companies like Medtronic and LivaNova PLC, focusing on device-based therapies, are heavily invested in solutions tailored to patients whose seizures stem from structural lesions or identified brain injuries. This strategic alignment toward the highest-revenue segment ensures that technological progress remains rapid and highly focused on the needs of this complex patient population, solidifying the symptomatic segment's leading position.

Furthermore, the significant revenue generated by this segment—accounting for 35% of the total—highlights the essential role of specialized healthcare centers, namely hospitals. These institutions, responsible for 70.4% of the end-user revenue, are the central hubs for the advanced diagnostic and surgical procedures required by symptomatic epilepsy patients. The rapid expansion of medical infrastructure in emerging markets, especially the Asia Pacific region, is increasing the capacity to treat these complex cases, thereby reinforcing the symptomatic segment's dominance. As global healthcare systems continue to battle the fallout from trauma and chronic neurological diseases, the financial and clinical importance of targeted solutions for symptomatic epilepsy will only continue to rise. This dynamic interplay between disease prevalence, advanced technology, and infrastructure capacity defines the current state and future direction of the global epilepsy market.

Categorie

Leggi tutto

"Regional Overview of Executive Summary Biomaterials Market by Size and Share A consistent market research report like Biomaterials Market report extends reach to the success in the business. This market research report takes into account plentiful aspects of the market analysis which many businesses demand. The winning market analysis report displays a professional and...

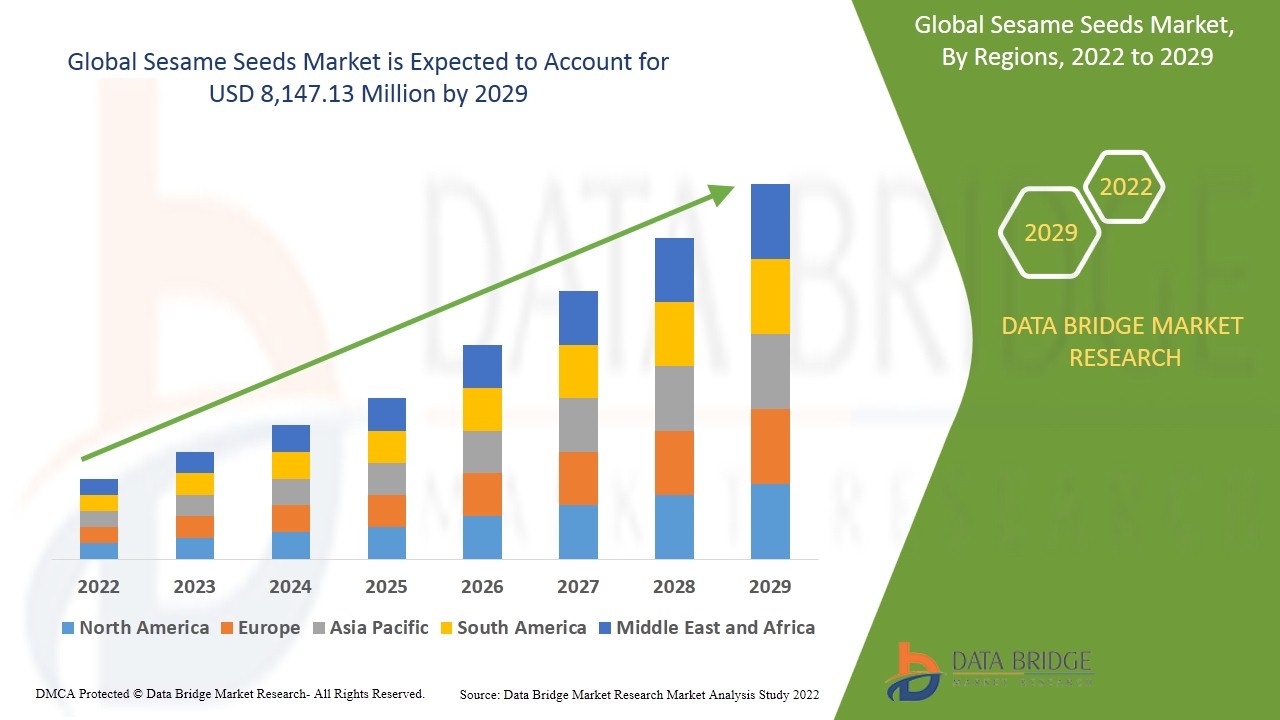

"Latest Insights on Executive Summary Sesame Seeds Market Share and Size CAGR Value Data Bridge Market Research analyses that the global sesame seeds market to be growing at a CAGR of 2.40% in the forecast period of 2022-2029 and is estimated to reach the USD 8,147.13 million by 2029. Objectives of the Market research are kept in mind while preparing the reliable Sesame Seeds...

"Undervale Hotel" Returns for Second Installment Netflix has officially greenlit the sophomore season of the popular adult animated series "Haunted Hotel," inviting viewers to check back into the supernatural establishment. The comedy follows the challenges of a single mom managing the Undervale, a unique hotel where spirits roam the halls. Her deceased brother, now among the ghostly...

"Executive Summary Glyoxal Market: Share, Size & Strategic Insights CAGR Value The global glyoxal market size was valued at USD 325.99 million in 2024 and is expected to reach USD 511.79 million by 2032, at a CAGR of 5.8% during the forecast period. Glyoxal Market report is structured with the best and advanced tools of collecting, recording, estimating...

The Report Cube which is one of the leading market research company in UAE expects the India Halal Cosmetics Market to grow at a CAGR of around 30% through 2032, as highlighted in their latest research report. The study provides an in-depth analysis of the emerging trends shaping the India Halal Cosmetics Market and offers detailed forecasts for its potential growth during...